# Урок 4: Авторегрессия

Авторегрессия — это модель временных рядов, которая использует наблюдения из предыдущих временных шагов в качестве входных данных для уравнения регрессии, чтобы предсказать значение на следующем временном шаге.

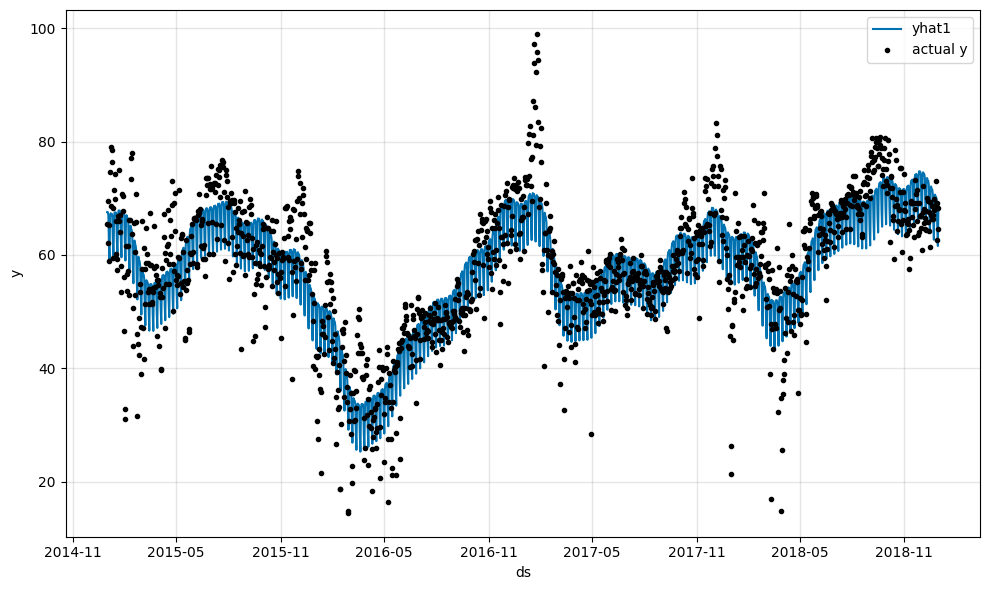

Мы начинаем с той же модели, что и в предыдущем учебнике.

```python

import pandas as pd

from neuralprophet import NeuralProphet, set_log_level

# Отключение сообщений журнала, кроме случаев ошибок

set_log_level("ERROR")

# Загрузка набора данных из CSV-файла с помощью pandas

df = pd.read_csv("https://github.com/ourownstory/neuralprophet-data/raw/main/kaggle-energy/datasets/tutorial01.csv")

# Модель и прогнозирование

m = NeuralProphet(

n_changepoints=10,

yearly_seasonality=True,

weekly_seasonality=True,

daily_seasonality=True,

)

m.set_plotting_backend("plotly-static")

metrics = m.fit(df)

forecast = m.predict(df)

m.plot(forecast)

```

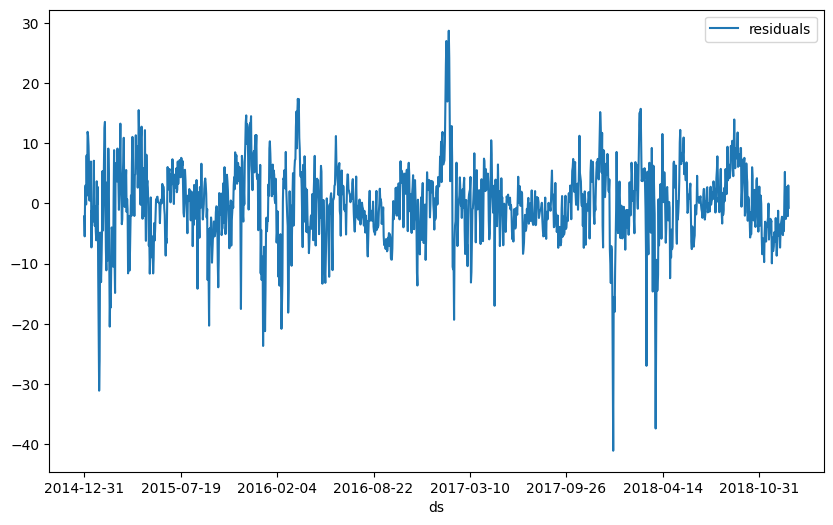

Чтобы лучше понять, в чем заключается оставшееся несоответствие между нашей моделью и реальными данными, мы можем посмотреть на остатки. Остатки представляют собой разницу между прогнозом модели и реальными данными. Если модель идеальна, остатки должны быть равны нулю.

```python

df_residuals = pd.DataFrame({"ds": df["ds"], "residuals": df["y"] - forecast["yhat1"]})

fig = df_residuals.plot(x="ds", y="residuals", figsize=(10, 6))

```

Давайте изучим, какое значение авторегрессии будет хорошим. Создайте график автокорреляции.

```python

from statsmodels.graphics.tsaplots import plot_acf

plt = plot_acf(df_residuals["residuals"], lags=50)

```

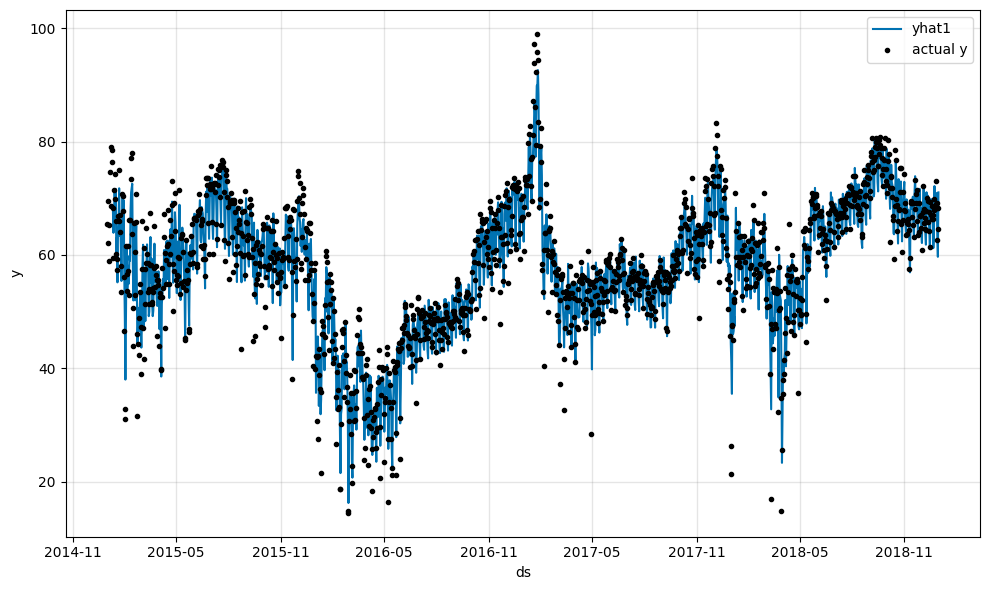

Теперь мы добавляем авторегрессию в нашу модель с параметром `n_lags`

```python

# Модель и прогнозирование

m = NeuralProphet(

# Отключение точек изменения тренда

n_changepoints=10,

# Отключение компонентов сезонности

yearly_seasonality=True,

weekly_seasonality=True,

daily_seasonality=True,

# Добавление авторегрессии

n_lags=10,

)

m.set_plotting_backend("matplotlib") # Использование matplotlib из-за #1235

metrics = m.fit(df)

forecast = m.predict(df)

m.plot(forecast)

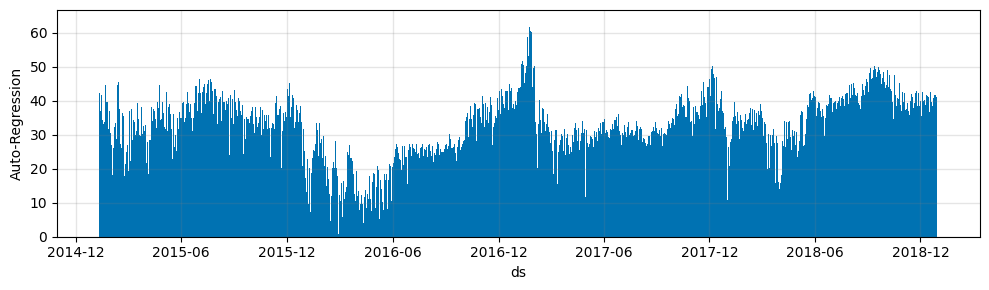

```

Как мы видим, модель прогнозирования с авторегрессией значительно лучше подходит к данным, чем базовая модель. Не стесняйтесь исследовать, как различное количество лагов `n_lags` влияет на модель.

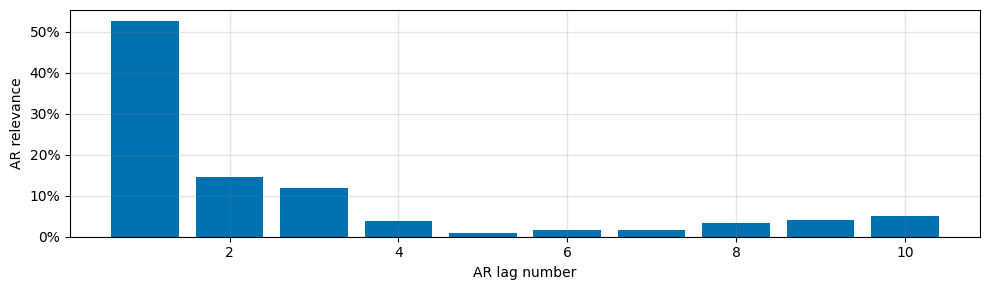

```python

m.plot_parameters(components=["autoregression"])

```

```python

m.plot_components(forecast, components=["autoregression"])

```

---

# Agent Instructions: Querying This Documentation

If you need additional information that is not directly available in this page, you can query the documentation dynamically by asking a question.

Perform an HTTP GET request on the current page URL with the `ask` query parameter:

```

GET https://bemind.gitbook.io/neural/neuralprophet/novye-uroki/urok-4-avtoregressiya.md?ask=

```

The question should be specific, self-contained, and written in natural language.

The response will contain a direct answer to the question and relevant excerpts and sources from the documentation.

Use this mechanism when the answer is not explicitly present in the current page, you need clarification or additional context, or you want to retrieve related documentation sections.